Buying a Home Without a Traditional Paycheck

Not every strong buyer fits neatly into a traditional mortgage box.

Some people own businesses.

Some are investors.

Some have strong assets but low taxable income on paper.

Others make great money through commissions, 1099 income, or multiple income streams that do not always show up cleanly on a standard loan application.

And honestly… that is more common than people think.

One of the biggest misconceptions in real estate is that if a buyer does not fit the traditional W-2 mold, they are automatically not qualified.

That is not always true.

Sometimes the issue is not whether someone can afford the home.

Sometimes the issue is simply finding the financing strategy that actually matches their real financial picture.

That is where non-traditional mortgage options and Non-QM lending can become valuable tools.

What Is a Non-QM Loan?

A Non-QM loan, short for non-qualified mortgage, is designed for buyers who may not fit traditional lending guidelines but still have the ability to purchase real estate responsibly.

Instead of relying only on a traditional W-2 and tax return, these programs can allow buyers to qualify using things like:

Bank statements

Assets

Rental income

1099 income

Alternative documentation

Investment property cash flow

And no, this does not mean “easy approval” or risky lending. Buyers still need to demonstrate financial strength and the ability to repay the loan. The difference is simply how the lender evaluates the financial picture. For many buyers, this creates opportunities that traditional financing may not.

When Traditional Financing Gets Tricky

Traditional mortgage guidelines work great for buyers with:

Consistent W-2 income

Straightforward tax returns

Simple financial structures

But life and business are not always that clean.

A business owner may write off expenses to reduce taxable income.

An investor may own multiple properties that create a complicated tax return.

A high-net-worth buyer may have substantial assets but not show large monthly income on paper. Ironically, some financially strong buyers can actually look weaker on a traditional mortgage application. That is where expanded lending solutions can help bridge the gap.

What This Can Look Like in Real Life

These situations are more common than people realize:

A business owner buying a home while self-employed

A commission-based professional with fluctuating income

A real estate investor purchasing another rental property

A buyer using bank statement loans instead of tax returns

Someone purchasing a home with 1099 income

A high-net-worth buyer living off investments instead of a salary

A homeowner wanting to buy before selling their current home

The financing strategy simply needs to match the buyer’s actual financial situation.

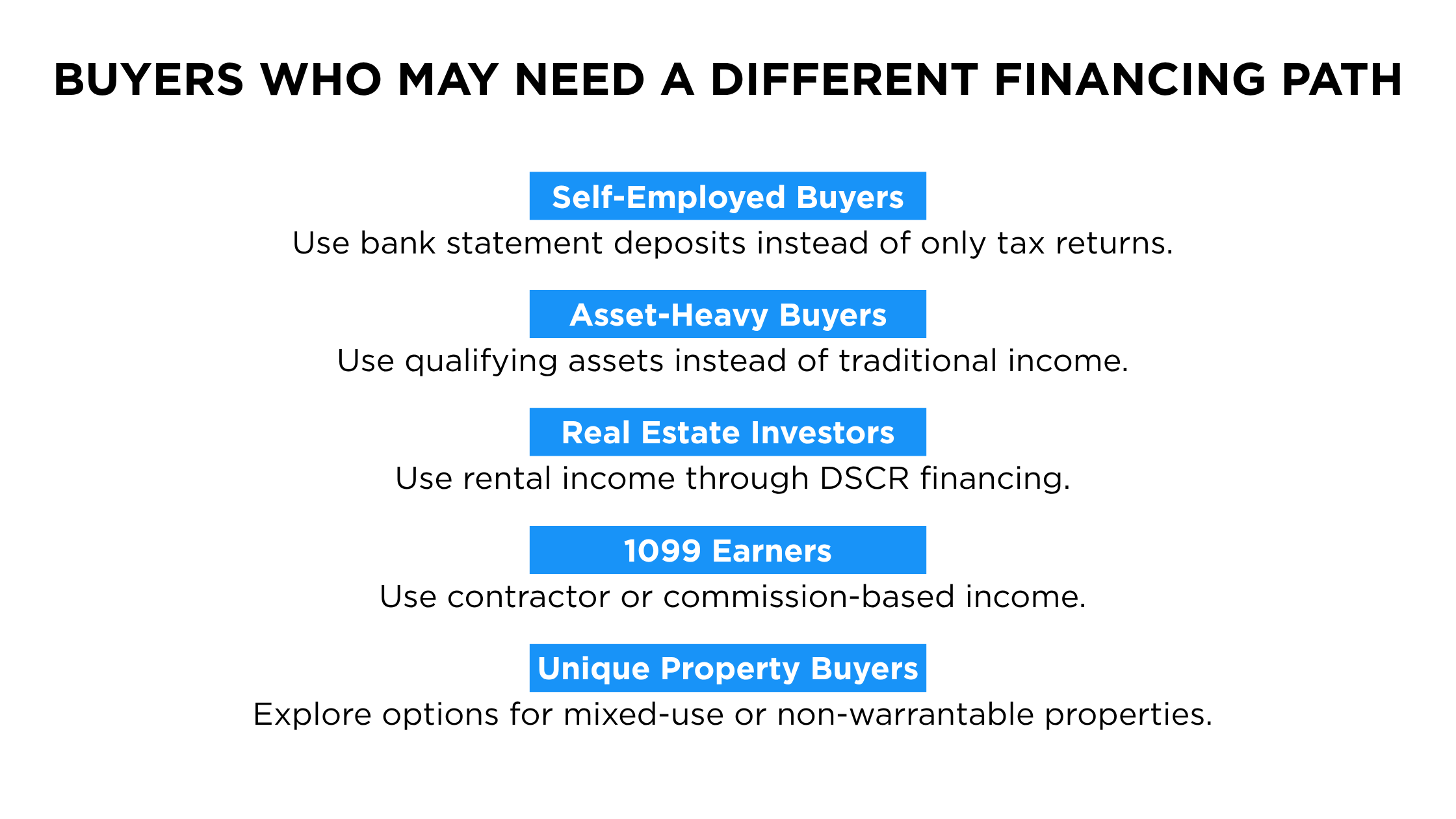

Options for Self-Employed Buyers

Self-employed buyers are some of the hardest-working people out there… but traditional lending does not always make the process easy.

For example, bank statement loans may allow buyers to qualify based on deposits over a 12- or 24-month period instead of relying only on tax returns.

This can be helpful for business owners, entrepreneurs, real estate professionals, independent contractors, gig-economy workers and commission based earners.

There are also home loan options for buyers with 1099 income whose earnings are strong but structured differently than a traditional employee paycheck.

Options for Buyers With Strong Assets

Some buyers have built wealth through:

Investments

Retirement accounts

Savings

Business ownership

Real estate portfolios

But they may intentionally keep taxable income lower as part of their overall financial strategy. Some lending programs allow buyers to qualify based more on assets than traditional income. In many situations, buyers do not need to fully liquidate those accounts either. That can help people avoid triggering taxes, disrupting investments, or changing a long-term financial plan simply to qualify for a mortgage.

Real Estate Investors Have Options Too

For investors, personal income is not always the best way to evaluate a purchase. A DSCR loan, which stands for Debt Service Coverage Ratio, focuses more on the rental income of the property than the borrower’s personal income.

In simple terms:

If the property cash flows well, the financing may work.

This can be a powerful option for investors growing a rental portfolio without having every purchase tied directly to their personal tax returns.

Sometimes the Property Creates the Challenge

Not every financing hurdle is about the buyer. Sometimes the property itself creates complexity. Maybe the buyer wants to purchase a new home before selling their current one.

Maybe the property is mixed-use. Maybe it is a non-warrantable condo or another unique property type that falls outside conventional lending guidelines.

These situations can feel frustrating if buyers only look at traditional mortgage options.

But alternative financing strategies can sometimes create flexibility where buyers thought they had none.

The Importance of Early Strategy Conversations

One of the biggest mistakes buyers make is assuming they are not qualified before having the right conversations.

Sometimes a different lending strategy can completely change what is possible.

That is one reason we like having early strategy conversations between the buyer, lender, and advisor from the beginning. It creates clarity around goals, financing options, timelines, and what path may make the most sense before emotions get too involved in the process.

Not every buyer needs a Non-QM loan.

But some buyers may have more options available than they realize.

In Conclusion

Every buyer’s story looks different.

The key is having a strategy that looks beyond just a tax return and understands the full picture. Because sometimes the difference between “not possible” and “let’s make a plan” is simply having the right team and the right lending approach from the beginning. And in real estate, that can make all the difference in helping people truly love where they live.